The 2020 Federal Budget, delayed by five months, prepared amidst a once-in-a-century pandemic that has ravaged the economy and up-ended so many norms of life, has now revealed the next chapter of this saga.

Over the last seven months, the Government’s priority has been to stem the damage necessarily inflicted upon ourselves because of COVID-19. Those measures include the JobKeeper program, Cash flow boost, JobSeeker supplement, business loan guarantee program, and other support measures. And they have largely done their job. Despite an effective unemployment rate (ie, including stood-down JobKeeper recipients) of over 9%, and the economy shrinking by an astonishing 7% in the June 2020 quarter alone, these results would have been a lot worse without those support measures.

However, those support measures are slowing phasing out, and minimising the down has come at a cost. With a budget deficit of $213.7 billion for 2020/21, and more over the next few years, the Government must now turn toward building the recovery out of the COVID-19 recession. And that’s where Budget 2020 comes in, featuring a number announced measures as part of the Government’s “JobMaker” plan.

We set out a summary of the key measures announced affecting business and high net worth individuals, and what they mean for you.

Talk to your trusted Focus advisor about what any of the Budget announcements mean for you or your business.

Individuals

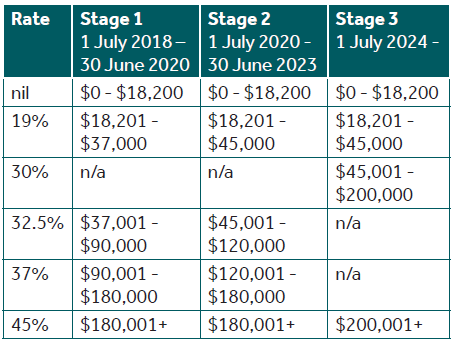

1. Income Tax Rate Cuts

Background

In the 2018 Federal Budget, the Government announced cuts to personal marginal tax rates, to be progressively phased in with the third and final stage taking effect from 1 July 2024.

Announcement

As a stimulus measure, the Government has now brought forward the second stage of the cuts that will now apply from 1 July 2020 instead of 1 July 2022.

The third stage of the cuts is unaffected by the Budget announcement.

The Government has not announced any changes to the Medicare Levy, currently levied at a flat rate of 2 per cent in addition to the marginal rates listed above.

Similarly, no change to the Medicare Levy Surcharge has been announced.

Some taxpayers may be exempt from the Medicare Levy and the Medicare Levy Surcharge.

What this means for you

The backdating of the tax rate cuts to 1 July 2020 means the change will have retrospective effect. Most salary and wage earners will see more money in their pay packet almost straight away after the change is legislated. Payroll software will need to be reconfigured to ensure the correct amount of PAYG tax is withheld, going forward.

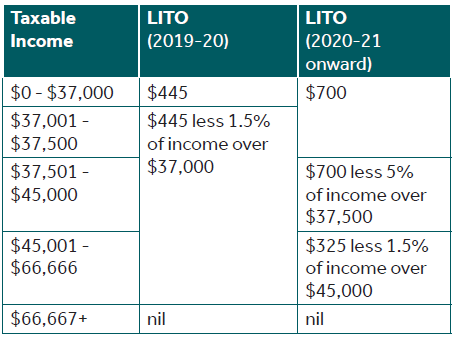

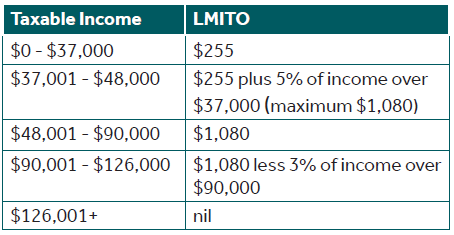

2. Low Income Tax Offset & Low and Middle Income Tax Offset

Background

The Low Income Tax Offset (LITO) is a rebate of tax available to individuals whose incomes are less than $66,667 in an income year.

The Low and Middle Income Tax Offset (LMITO) is a further rebate of tax available to individuals whose incomes are less than $126,000 in an income year.

Announcement

The planned increase in the maximum annual rebate available under LITO from $445 to $700 per year, previously scheduled for introduction in the income year ending 30 June 2023, will be brought forward to the current income year, based on the following schedule:

The LMITO was scheduled to cease with the introduction of Stage 2 of the cuts to personal income tax rates on 1 July 2022. Stage 2 has been brought forward, with effect from 1 July 2020, however the LMITO will be retained for the current income year, with the existing maximum rebate retained at $1,080 based on the following schedule:

What this means for you

The rebate becomes available upon lodgement of the individual’s tax return.

3. Exempting Granny Flat Arrangements from Capital Gains Tax

Background

Capital gains tax (CGT) may apply to the creation, variation or termination of a formal written granny flat arrangement which enables accommodation for older Australians or people with disabilities. The granting of a right to occupy a property for life or a certain term is a taxing event and the ensuing taxable capital gain may be the present value of the right to receive income over many years – this could amount to many thousands of dollars.

Announcement

The Government has decided that CGT will not be payable where a formal written agreement is entered into with an older or disabled Australian.

What this means for you

Children will now be able to accommodate older parents or disabled relatives under a formal written lease agreement without being subject to CGT. This is expected to encourage accommodation arrangements for older and disabled Australians and reduce financial abuse of such people.

Date of Effect

This measure will have effect from the first income year after the date of Royal Assent of the enabling legislation.

Businesses

1. JobMaker Hiring Credit

Background

The Government’s approach throughout the COVID-19 pandemic has been predominantly to support maintenance of private sector employment. This is now pivoting to supporting the creation of new employment.

Announcement

The Government will encourage employment growth over three years by providing a hiring credit to eligible employers who take on additional eligible employees. The credit will be provided for 12 months for each eligible new hire that increases overall employee headcount from a reference date of 30 September 2020. The credit will be $200 per week for eligible employees hired aged 16 to 29 years, and $100 per week where aged 30 to 35 years. The maximum credit receivable for an employee is $10,400 ($200 x 52 weeks).

To be an eligible employee, the individual will need to have worked 20 or more hours per week, averaged over a quarter, and received JobSeeker, Youth Allowance (Other) or Parenting Payment for at least one month out the three months prior to being hired.

To be an eligible employer, amongst other requirements, tax lodgements must be up to date, report through Single Touch Payroll, and have kept adequate records.

What this means for you

Where your business needs to hire new employees, there is an incentive to prefer those who would qualify as an eligible employee. Receipts such as these are usually assessable income to your business, unless specifically exempted. No mention has been made yet on whether the credit will be made tax exempt.

2. Extension of Small Business Concessions

Background

A Small Business Entity is currently defined as business with group-wide turnover of less than $10 million, which entitles them to a series of concessions for income tax, FBT, and GST.

Announcement

The turnover threshold to be a Small Business Entity will be increased to $50 million, with access to the concessions in three phases:

- 1 July 2020 in respect to the immediate deduction of:

a. certain business start-up expenses

b. prepayments - 1 April 2021 in respect of the exemption from FBT:

a. for car-parking; and

b. provision of more than one work-related portable electronic device - 1 July 2021 in respect of:

a. Simplified trading stock rules;

b. Making PAYG Instalments based on GDP adjusted notional tax;

c. Two-year amendment period;

d. Monthly payment of excise duty and excise-equivalent customs duty on eligible goods

The Commissioner of Taxation will also be given the power from 1 July 2021 to issue a Simple GST accounting method determination for businesses with a turnover of less than $50 million.

What this means for you

Around 20,000 more businesses will be able to use these concessions to reduce their costs of complying with their tax obligations. The $50 million turnover threshold will also now align with the threshold for the lower 26% company tax rate.

3. Temporary full expensing of eligible depreciable assets

Background

Prior to COVID-19 (pre 12 March 2020) the instant asset write-off incentive enabled businesses with a group-wide turnover of less than $50 million to immediately deduct the cost of depreciating assets that cost less than $30,000 (net of GST credit).

In response to COVID-19, the Government expanded the eligibility by increasing the group-wide turnover threshold from $50 million to $500 million, and increased the cost threshold limit to under $150,000. These rules applied from 12 March 2020 until 31 December 2020.

Announcement

The instant asset write-off will be further expanded whereby businesses with a group-wide turnover of less than $5 billion can deduct the full cost of eligible assets acquired from 7.30pm AEDT on 6 October 2020 until 30 June 2022. This is available on new depreciable assets and the cost of improvements to existing eligible assets. These rules also apply to second-hand assets if group-wide turnover is less than $50 million.

Businesses with an aggregated turnover of between $50million and $500 million can still deduct the full cost of eligible second-hand assets costing less than $150,000 provided they are purchased before 31 December 2020 and first used or installed by 30 June 2021.

Small businesses with group-wide turnover of less than $10 million can deduct the balance of their small business pool at the end of the income year while the full expensing applies.

What this means for you

These enhanced rules will enable businesses to deduct the full cost of asset in the year they are first used or installed ready for use. This incentive brings forward the deduction that you would have received in future years (ie a timing difference) and allows for a cash flow benefit to be received sooner rather than later.

We note that the best reason to acquire any new asset is not a tax write-off, but rather the judgement that your business will earn a sufficient commercial return from investing in that asset. The full tax deduction is merely a timing difference – you would normally deduct the cost over several years anyway – and should be viewed more as a bonus to the commercial return.

4. Temporary Tax loss “carry-back”

Background

Currently, companies incurring tax losses must carry those losses forward and offset them against future years’ profits. Thus, any tax saving is not realised until that future time when the company is again profitable.

Announcement

The Government will allow companies with group-wide turnover of less than $5 billion to offset tax losses incurred in the 2019-20, 2020-21 or 2021-22 income years against prior year profits (from the 2018-19 year or later) on which they have previously paid tax. This will generate a refundable tax offset, available when lodging company tax returns for 2020-21 and 2021-22 years.

The amount to be “carried-back” however, will be limited to the amount of the taxable profit in that prior year and must not generate a franking account deficit.

What this means for you

This measure will provide much needed cash flow support to what were previously profitable companies that now find themselves in a tax loss position because of the COVID-19 pandemic. It also provides an incentive for companies to take advantage of the abovementioned full expensing measures while they are available.

The following example illustrates the benefits of these measures.

Smith Builders Pty Ltd has group-wide turnover of $60 million for the 2021-22 year. On 1 July 2021, the company purchases a new deliveries truck for $500,000 (excluding GST). Smith Builders Pty Ltd’s taxable income for the 2021-22 year is $300,000 before the purchase. Without full expensing, the company would claim a depreciation deduction of approximately $70,000, resulting in a taxable income of $230,000 and tax payable at 30% of approximately $69,000.

Instead, under the full expensing measures, Smith Builders will be able to claim a full tax deduction for the $500,000, resulting in a tax loss of $200,000. Under the tax loss carry back, Smith Builders offsets this loss against profits from 2018-19 year resulting in a tax refund at 30% of $60,000.

The combination of the full expensing and loss carry-back measures results in $129,000 ($69k + $60) additional cash available.

5. Wage subsidy for new apprentices

Background

In March, a wage subsidy commenced to support maintaining apprentice employment. It was due to end in September, but has been extended to July next year. However, this subsidy applies only to existing employed apprentices, and is available only for businesses with fewer than 20 employees.

Announcement

From 5 October 2020, employers will be eligible for a 50% wage subsidy for new or recommencing apprentices. The subsidy is 50% of the apprentice’s wages, up to $7,000 per quarter. Employers of any size or industry will qualify. The subsidy will be available until 30 September 2021.

What this means for you

Irrespective of any subsidy, there must be a business case to take on a new employee. However, the point of temporarily subsidising the cost of employment is to tip a business with a borderline or lesser business case into hiring a new apprentice earlier. The information released also states that the program will run until a target cap of 100,000 new apprentices is achieved. It is unclear if the subsidy will cease before 30 September 2021, should the cap be reached before then.

6. FBT Exemption for Employers and a Tax Deduction for Employees for Skills Training

Background

An employer does not pay FBT on providing their employees with skills training in circumstances where the employee would have been able to claim a tax deduction if they had instead paid for the training.

An employee is currently entitled to a tax deduction where the training relates to their current income-earning activities. For example, a sales assistant who undertakes a web-design course with the aim of obtaining an online marketing position with their current employer is unable to claim a tax deduction even though the course leads to higher income with their current employer. If the employer paid for providing the web-design training in this situation, FBT would be payable.

Announcement

Retraining and reskilling provided by an employer to their redundant or soon-to-be-redundant employees from 2 October 2020, possibly to enable the employees to be redeployed to a different role within the business, will be exempt from FBT.

The exemption will not apply to salary sacrifice arrangements or for training provided through Commonwealth-supported university places.

The Government has also announced that consultations will be undertaken with view of amending the tax law to allow workers to claim a tax deduction for self-education expenses that do not relate to their current income-earning activities.

What this means for you

This means that employers will be able to provide assistance to their employees to retrain and reskill them without being liable for FBT.

Employees may also be able to claim a wider range of self-education expenses not related to their current employment, thus reducing the cost of reskilling and retraining.

7. JobMaker Plan – Research and Development Tax Incentive

Background

Currently, the R&D Tax Incentive states that companies with a group-wide annual turnover of less than $20 million that are not controlled by exempt entities receive a refundable tax offset for R&D expenses of 43.5% and other companies receive a tax offset for R&D expenses of 38.5%.

However, a Bill is currently before the Senate Economics Legislation Committee that proposes major changes to the R&D Tax Incentive retrospectively for income years after 1 July 2019.

This Bill proposes:

- A refundable tax offset rate of the relevant corporate income tax rate plus 13.5% for companies with group-wide annual turnover of less than $20 million that are not controlled by exempt entities, with the cash tax refund to be limited to $4 million;

- A tax offset rate of the relevant corporate income tax rate plus intensity premiums for larger companies; and

- To increase the maximum R&D expenditure threshold from $100 million to $150 million.

Announcement

All changes to the R&D Tax Incentive will apply to income years starting on or after 1 July 2021. Retrospective changes for income years after 1 July 2019 will not be proceeded with.

Companies with group-wide annual turnover of less than $20 million will receive a refundable tax offset for R&D expenses of their corporate tax rate plus 18.5% (i.e. this will restore the existing rate of 43.5% because the corporate tax rate for smaller companies will be cut to 25% in the 2022 income year). There will be no cap on the annual cash tax refund.

Companies with an aggregated annual turnover of greater than $20 million will still be required to calculate their R&D tax offset rate based on their corporate income tax rate plus intensity premiums but the calculation of the intensity premiums is both simpler and significantly more generous. R&D intensity is R&D expenditure as a proportion of total expenses for the income year. The intensity premium for R&D expenditure of 0-2% R&D intensity is 8.5% and the intensity premium for R&D expenditure of over 2% R&D intensity is 16.5%.

The maximum R&D expenditure threshold will be increased from $100 million to $150 million.

The Government also will proceed with other technical measures as previously announced.

What this means for you

Companies are no longer exposed to unfavourable retrospective legislation because all changes will only apply for income years starting on or after 1 July 2021.

Companies with group-wide annual turnover of less than $20 million will now see minimal change to the calculation of their refundable tax offset, although we note that the rate of offset is being maintained even though the tax rate is being cut.

Larger companies with R&D intensity of over 2% and/or total R&D expenditure over $100 million should be able to claim a greater R&D tax offset going forward.

Superannuation

1. Superannuation Reform - YourSuper Portal

Background

Compulsory superannuation in Australia has resulted in a plethora of providers in the marketplace, some of which are underperforming. In addition, many Australians have more than one superannuation account, thereby duplicating fees paid.

Announcement

The Government has announced they will invest $159.6 million over four years to implement reforms to improve outcomes for superannuation fund members. New employees will be able to select a super fund from a table of products through the YourSuper portal.

A member’s super account will be ‘stapled’ to them, meaning it will follow them when they change employment.

From July 2021 the Australian Prudential Regulation Authority will conduct benchmarking on super products, with those underperforming over two consecutive annual tests not being allowed to accept new members. The results will be published.

What this means for you

The amount of multiple accounts that many Australians have will reduce and it will be easier to maintain one account, meaning unnecessary fees paid to providers will also reduce. The risk of fund balances for members being “lost” will decrease, thereby providing better outcomes for retirement.

Employers will probably not be able to just establish a new account for a new employee in their default fund, but will need to identify the superannuation account that has been attached the employee.