The forecast deficit for the 2022-23 year is $78 billion, and the current year’s deficit is expected to come in at $79 billion. These are significantly lower than forecast in the two previous Budgets.

Although some direct support measures continue, most have ceased. However, deficits and debt with be with us for many years, but that is the price of averting what might have been far worse.

Individuals

1. Low-and-Middle-Income Tax Offset

Background

The Low-and-Middle-Income Tax Offset (LMITO) is a non-refundable tax rebate which, as the name suggests, is available to low-to-middle income earners. This rebate reduces tax payable but cannot result in a tax refund.

Announcement

The Government has announced that the maximum amount of the rebate will increase from $1,080 to $1,500 for individuals and $3,000 for couples for the income year ending 30 June 2022. The purpose of the LMITO is to reduce cost of living increases.

All LMITO recipients will be entitled to the full $420 increase. Individuals earning less than $25,000 will not require the full additional rebate to pay no tax. Individuals with taxable incomes between $48,000 to $90,000 will receive the maximum rebate of $1,500. For individuals with taxable incomes between $90,001 and $126,000, the rebate tapers to $420 for individuals with a taxable income of $126,000.

What this means for you

Eligible individuals will now be entitled to a rebate of up to $1,500 upon lodgement of their individual income tax returns for the year ending 30 June 2022.

2. Cost of living–temporary fuel excise reduction

Announcement

The rate of the levy on petrol and diesel fuels will be halved from 30 March 2022 to 28 September 2022.

The excise and excise-equivalent customs duty rates for all other fuel and petroleum based products, except aviation fuels, will also be reduced by 50 per cent for the same period.

What this means for you

In simple terms, bowser prices should be 22.1 cents per litre less than they otherwise would be, plus an additional reduction in GST.

For example, a litre of petrol that cost $2.20 before this change (including 44.2 cents of excise levy and 20 cents in GST) should theoretically fall to $1.96 (including 22.1 cents of excise levy and 17.79 cents in GST).

The Australian Competition and Consumer Commission will play their role in ensuring the impact of these changes are passed on to the bowser price.

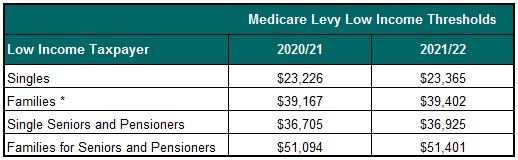

3. Increasing the Medicare Levy Low-Income Thresholds

Announcement

From 1 July 2021, the Government will increase the Medicare levy low-income thresholds for the below listed taxpayers. The changes reflect movements in the consumer price index.

* The family income threshold will be increased by a further $3,619 for each dependent child or student compared to the previous amount of $3,597.

What this means for you

Low-income taxpayers will continue to be exempt from paying the Medicare levy.

Eligibility for the threshold applies when the taxpayer has lodged their individual income tax return for the year ending 30 June 2022.

Businesses

1. Cashflow support and red tape reduction for small business

Announcement

A number of changes are intended to ease the cashflow burden for small business in complying with these obligations, and improve the use of technology for a more efficient administration. These include:

- Decrease the PAYG instalment uplift rate from 10% to 2%, effective from 1 July 2022.

- Implement new systems from 1 January 2024 that will enable automated calculation of PAYG instalments based on business performance.

- Share Single Touch Payroll (STP) data with state and territory governments, enabling pre-filling of payroll tax returns.

- Automated reporting drawn from activity statements to displace the annual Taxable Annual Payment Report (TPAR). This affects businesses in the construction, cleaning, road freight and courier services, information technology, and security, investigation and surveillance industries.

- From 1 July 2023, manufacturers, importers and distributors in the alcohol and fuel sectors with turnover below $50 million can lodge and pay excise and equivalent customs duty on a quarterly basis, instead of monthly or weekly.

What this means for you

Any improved use of technology and information sharing to reduce or eliminate duplication, or more seamlessly complete compliance obligations, is to be welcomed.

The change arising from reducing the PAYG instalment uplift rate is more limited, as tax instalments can be varied down in any case. This might also leave business owners with a deferred final tax payment. As always, managing cashflow, of which income tax obligations are a significant component, is a constant challenge for any business.

2. Extended wage subsidy for apprentices

Announcement

Any business receiving the BAC subsidy will be eligible for extended support through the Completing Apprenticeships Commencements (CAC) subsidy. This will continue until 30 June 2022. These subsidy programs have provided the following subsidies:

- 50 per cent of the apprentice’s wages in the first year, capped at a maximum payment value of $7,000 per quarter per apprentice,

- 10 per cent of the apprentice’s wages in the second year, capped at a maximum payment value of $1,500 per quarter per apprentice, and

- 5 per cent of the apprentice’s wages in the third year, capped at a maximum payment value of $750 per quarter apprentice.

What this means for you

Irrespective of any subsidy, there must be a business case to take on a new employee. However, the point of temporarily subsidising the cost of employment during the pandemic is to tip a business with a borderline business case into hiring a new apprentice earlier.

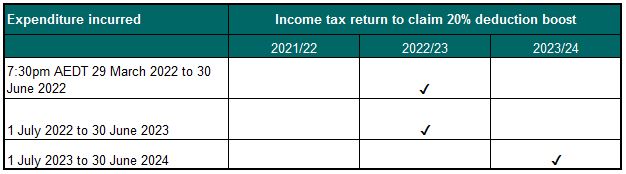

3. 120% deduction for skills and training expenditure

Announcement

Businesses with group-wide turnover below $50 million will be entitled to a bonus 20% tax deduction for expenditure incurred on external training courses provided to their employees.

To qualify, the training courses must be:

- provided to employees in Australia or online

- delivered by a training provider registered in Australia

- expenditure that is incurred from 29 March 2022 to 30 June 2024

There will be some exclusions such as in-house or on-the-job training. It will also exclude training courses for persons other than employees. For eligible expenditure incurred up to 30 June 2022, the 20 per cent boost deduction component will deductible in the 2022-23 income year. The 20 per cent boost for eligible expenditure incurred in the 2022-23 and 2023-24 income years will be deductible in the year in which the expenditure is incurred.

What this means for you

As a small business, investments made in the upskilling of your employees may entitle you to an additional 20% tax deduction in respect of eligible expenditure incurred.

There is no limit on the amount of eligible expenditure.

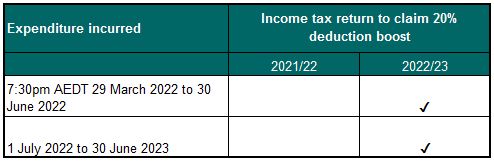

4. 120% deduction for technology investment expenditure

Announcement

The Government is introducing a more targeted incentive to support digital adoption by small businesses. The boost will apply to eligible expenditure incurred from 7.30pm AEDT on 29 March 2022 until 30 June 2023.

Businesses with group-wide turnover below $50 million will be able to deduct an additional 20 per cent of the cost of business expenses and depreciating assets that support their digital adoption. The additional deduction will be subject to an eligible expenditure cap of $100,000.

The technology investment boost will support digital investments such as cloud computing, cyber security systems, web page design, e-invoicing software and portable payment devices.

For eligible expenditure incurred up to 30 June 2022, the 20 per cent boost deduction component will deductible in the 2022-23 income year. The 20 per cent boost for eligible expenditure incurred in the 2022-23 income year will be deductible in that same year.

What this means for you

With no further extension to the temporary full expensing of eligible depreciable assets, businesses with group-wide turnover below $5 billion will be able to deduct the full cost of eligible assets acquired from 7.30pm AEDT on 6 October 2020 until 30 June 2023 as per existing laws.

But now, in addition to the above, businesses with group-wide turnover below $50 million will be able to deduct this bonus 20 per cent of eligible expenditure.

The 20 per cent boost is claimable as follows:

For example, if eligible expenditure of $100,000 is incurred by 30 June 2022, and a further $100,000 by 30 June 2023, a total bonus deduction of $40,000 ($200,000 x 20%) would be claimable in the 2022-23 income year, reducing a company’s tax liability by $10,000 (25% company tax rate)

There will inevitably be administrative costs to comply with the necessary record-keeping.

5. Export Market Development Grant & Regional Accelerator Program

Announcement

Following the opening of Australia’s international borders, the Government will supply a further $80 million in EMDG to assist businesses to re-establish their presence in overseas markets and be better able to export their products and services.

The Government is also establishing the Regional Accelerator Program (RAP), at a cost of $2 billion, to drive economic growth and productivity in regional areas. The 5-year program will commence on 1 July 2022 and will fund programs targeted at improving infrastructure, manufacturing, industry development, research and development and education in regional areas.

What this means for you

Businesses intending to market their goods and/or services overseas should consider their eligibility for the EMDG. EMDG applications are due by 30 November 2022, for the year ending 30 June 2022.

6. Employee Share Schemes – greater access, less red tape

Announcement

The Government will now allow unlisted entities to claim relief from disclosure requirements for offers under an ESS where they make offers of up to:

- $30,000 per participant per year, with unexercised options accruing for up to 5 years in addition to 70% of dividend and cash bonuses; or

- any amount if the offer allows participants to immediately take advantage of a planned sale or listing of a company.

The Government will also remove the restriction on relief for offers under an ESS to contractors.

What this means for you

This will increase the availability of relief for employers in relation to the reporting and disclosure obligations for an ESS and reduce the corresponding compliance burden. Employees will benefit from being able to share in business growth and profits by participating in an ESS.

7. Primary producers – farm management deposits and carbon credits

Background

Farm Management Deposits (FMD) allow primary producers to smooth out their tax liabilities across multiple years by making tax deductible contributions in high-income years, and assessable withdrawals in low-income years.

Currently, proceeds from selling Australian Carbon Credit Units (ACCUs) are treated as non-primary production income and are generally ineligible for contribution to a FMD. Also, ACCU holders are taxed based on changes in the value of their ACCUs each year, which can result in tax liabilities prior to sale.

Announcement

From 1 July 2022, the Government will allow the proceeds from the sale of ACCUs and biodiversity certificates generated from on-farm activities to be treated as primary production income. Accordingly, the proceeds can be contributed to a FMD.

The Government will also change the taxing point of ACCUs for eligible primary producers to the year when they are sold.

What this means for you

This change enhances primary producers’ ability to manage their tax liabilities, and aligns income tax liabilities on ACCUs with when they are actually sold.

8. ATO Tax Avoidance Taskforce additional funding

Background

The Government established the ATO’s Tax Avoidance Taskforce in 2016 to undertake reviews and audits of multinationals, large public and private groups, trusts, and high wealth individuals.

The Taskforce’s programs include:

- Justified Trust;

- Medium & Emerging Private Groups;

- Top 500 private groups tax performance program;

- Top 1000 public groups performance program;

- High risk trusts;

- Medium & Emerging Private Groups.

The Taskforce has recovered $12.7 billion in taxes from 1 July 2016 to 30 June 2021.

Announcement

The Taskforce will be extended for a further two years, to 30 June 2025, at a cost of $652.6 million. The Taskforce is expected to collect at least $2.1 billion in otherwise unpaid taxes.

Superannuation

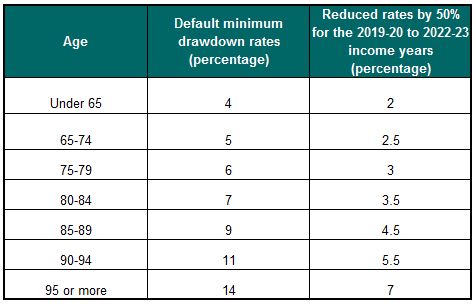

1. Temporary reduction in superannuation minimum drawdown rates extended

Background

When a self-funded retiree commences a pension, they are required to withdraw a minimum amount annually based on their prior year member balance.

Announcement

To ensure stability in superannuation for self-funded retirees, the Government has announced an extension of the current 50 per cent temporary reduced minimum pension amount for a further year to 30 June 2023.

This will apply to account-based pensions (including transition to retirement income streams), and market-linked pensions. It will not apply to defined benefit income streams.

What this means for you

The 50 per cent reduction of the minimum drawdown requirements for account-based pensions and market-linked pensions will continue to 30 June 2023. The relevant rates are below.

Talk to your trusted Focus advisor about what any of the Budget announcements mean for you or your business.