Relevant Tax Guide to the Federal Budget 2023

Treasurer Jim Chalmers has delivered his second Budget. We set out a summary of the key measures announced, and what they mean for you and your business.

INDIVIDUALS

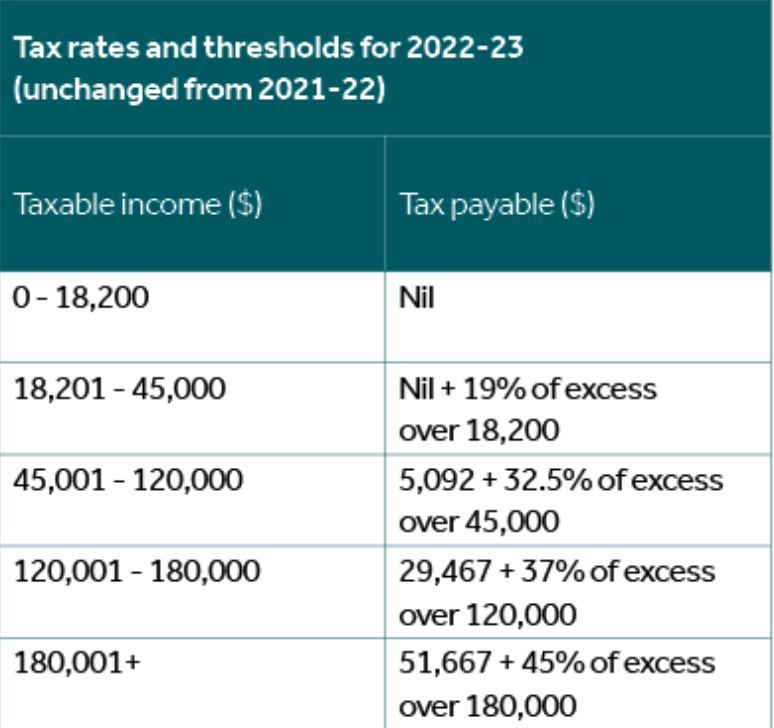

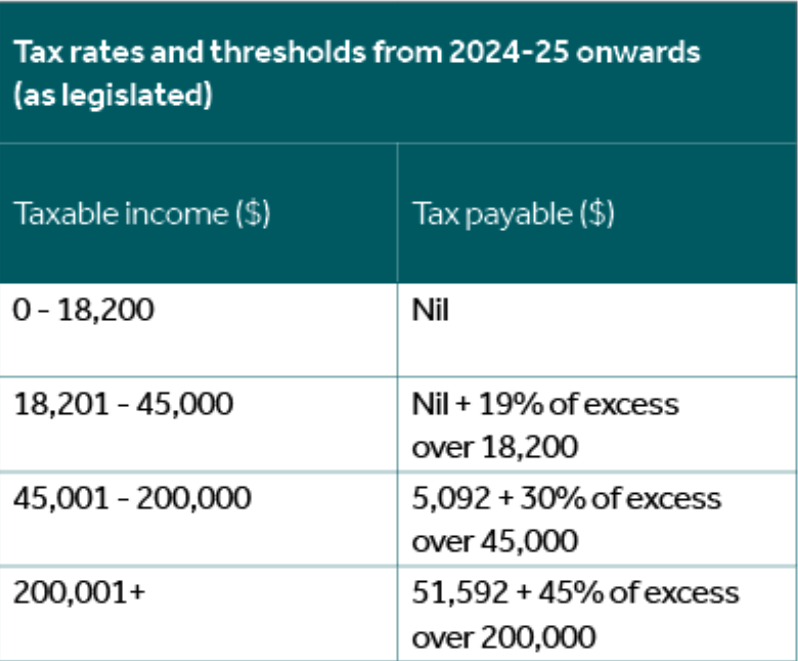

No changes to personal tax rates

The Government has again left the previously legislated personal tax rate changes unchanged. With no announcement of any changes to the personal tax rates, the Stage 3 tax changes will commence from 1 July 2024, as legislated. Under the Stage 3 tax changes, the 32.5% marginal tax rate will be reduced to 30% for the income bracket between $45,000 and $200,000. The 37% tax bracket will be completely removed from the 2024-25 income year. This means that the following individual income tax rates will apply (excludes the 2% Medicare levy):

Low-and-middle-income tax offset not extended

No further extension of the LMITO was announced in this Budget. As such, the LMITO has now ceased (with the 2021-22 income year being the final year), and now replaced by the low-income tax offset.

Cost-of-living relief

Eligible beneficiaries, including pensioners, small businesses, and individuals receiving income support, will have their bills subsidized by up to $500. The extent of the support is dependent on which state or territory the recipient lives in.

BUSINESS

Instant Asset Write-Off Threshold of $20,000 for Small Business

Small businesses (group-wide turnover less than $10 million) currently benefit from an unlimited instant asset write-off which is due to end on 30 June 2023. The Government will temporarily retain an instant asset write-off for the full cost of eligible assets costing less than $20,000 (excluding any GST credit) that are first used or installed for use between 1 July 2023 and 30 June 2024. The threshold of $20,000 will apply on a per-asset basis. Effectively, small businesses will be able to claim a tax deduction for the full cost of multiple assets. Assets costing $20,000 or more (which cannot be immediately deducted) can continue to be placed into the small business simplified depreciation pool and depreciated at 15% in the first income year and 30% each income year thereafter.

Small business energy incentive

Businesses with an annual turnover of less than $50 million will receive an additional 20% deduction on investments that support energy-efficient practices and implementing energy-saving technologies. The purpose is to encourage making investments like electrifying heating and cooling systems, upgrading to more efficient fridges and induction cooktops, and installing batteries and heat pumps. The measure is part of a larger push to ensure that small business operators can share in the energy transition that is now underway, whilst also helping Australia lower its emissions. Up to $100,000 of total expenditure will be eligible, allowing a maximum bonus tax deduction of $20,000 per business. Eligible assets or upgrades will need to be installed and ready for use between 1 July 2023 and 30 June 2024 to qualify for the bonus 20% deduction.

Petroleum Resource Rent Tax and Mining, Quarrying and Prospecting Rights

Under the current rules, most LNG projects are not expected to pay significant amounts of PRRT until the 2030s. From 1 July 2023 or seven years after the date of first production, whichever is the later, the Government will limit the proportion of PRRT assessable income of LNG projects that can be offset by most deductions to 90 per cent. That is, 10% of PRRT income from LNG projects will not be able to be reduced by most deductions. This means that some petroleum resource rent tax at least should generally be payable within seven years of an LNG projects date of first production.

No new tax concessionary regime for income from patents

The previous Government had announced that a concessionary patent box regime would be introduced under which income from certain kinds of patents would be taxed at a lower rate. The current Government has announced that they will not be proceeding with this measure.

Reduction of Statutory GDP Adjustment Factor for PAYG and GST Instalments

The ATO calculates PAYG and GST Instalments using information from the previous years tax return which is indexed using a GDP Adjustment Factor to account for any likely growth in income from the prior year. The statutory GDP Adjustment Factor has been reduced to 6% for the 2023-24 income year, halving the 12% which would have applied under the statutory formula.

Lodgment penalty amnesty for small businesses

In an effort to encourage small businesses with outstanding tax statements to re-engage with the ATO, the Government has announced that it will provide a temporary lodgment penalty amnesty to small businesses with group-wide turnover of less than $10 million. The amnesty will remit failure-to lodge penalties for outstanding tax statements lodged in the period from 1 June 2023 to 31 December 2023 that were originally due during the period from 1 December 2019 to 29 February 2022.

Increase in heavy vehicle road user charge

The federal government will raise the heavy vehicle road user charge by six percent each year for the next three years. The charge relates to each litre of diesel used by heavy vehicles and will come into effect on June 1.

SUPER ANNUATION

Employer Payday Super Obligations

From 1 July 2026, employers will be required to pay an employees superannuation at the time that they pay their wages. This change will affect all employers, but the Government has provided a three-year lead-in period in order to allow employers adequate time to adjust their systems accordingly.

Additional Resourcing to Enforce Superannuation Compliance

The Government is providing more resourcing to the ATO to enable them to detect unpaid employer superannuation obligations earlier. In addition, the ATO will be set enhanced targets for the recovery of all such unpaid superannuation for employees. The underlying message here is that employers who are not up to date with their employee superannuation obligations face a heightened risk of detection, which comes with significant penalties.

Additional tax on higher super account balance

From 1 July 2025, an additional 15% tax on the earnings will apply to individuals with a Total Superannuation Balance (TSB) of more than $3 million on any subsequent 30 June. Earnings for this purpose will be calculated using a formula, reflecting the change in the value of the TSB at the start and end of the financial year, excluding the effect of withdrawals and contributions. This means that any unrealised gains and losses will be included in the calculation. The $3 million threshold applies to individuals of all ages, even if an individual is not eligible to access their superannuation benefits. The additional tax will be assessed to the individual, who can pay it personally, or choose for the tax to be paid from their superannuation fund. Individuals with a TSB balance of less than $3 million at 30 June in a year will not be affected.

Non-arms length income

From 1 July 2023, an effective tax rate of 90% will apply to self-managed superannuation funds (SMSFs) or a small APRA-regulated funds (with 6 or fewer members) in relation to certain expenses. Under the non-arms length income (NALI) provisions, if the fund incurs a general expense that is not at arms length terms, the punitive tax impost applies to the taxable income equivalent to the shortfall amount.

Talk to your trusted Focus Professional Group advisor about what any of the Budget announcements mean for you or your business.